Related Articles

Whether you use an app or a budget worksheet to get a handle on your spending, you’ll want to know where your money is going — and then make a plan for where you want it to go.

The 50/30/20 budget is a good tool to do just that.

Use our calculator to estimate how you might divide your monthly income into needs, wants and savings. This will give you a big-picture view of your finances. The most important number is the smallest: the 20% dedicated to savings. Once you achieve that, perhaps with an employer-sponsored retirement plan and other automated monthly savings transfers, the rest — that big 80% chunk — is up for debate.

That leaves 50% for needs and 30% for wants, but these are parameters you can tweak to suit your reality. For example, if you live in an expensive housing market, your monthly mortgage or rent payment might spill a bit into your “wants” budget. Budgets are meant to bend but not be broken.

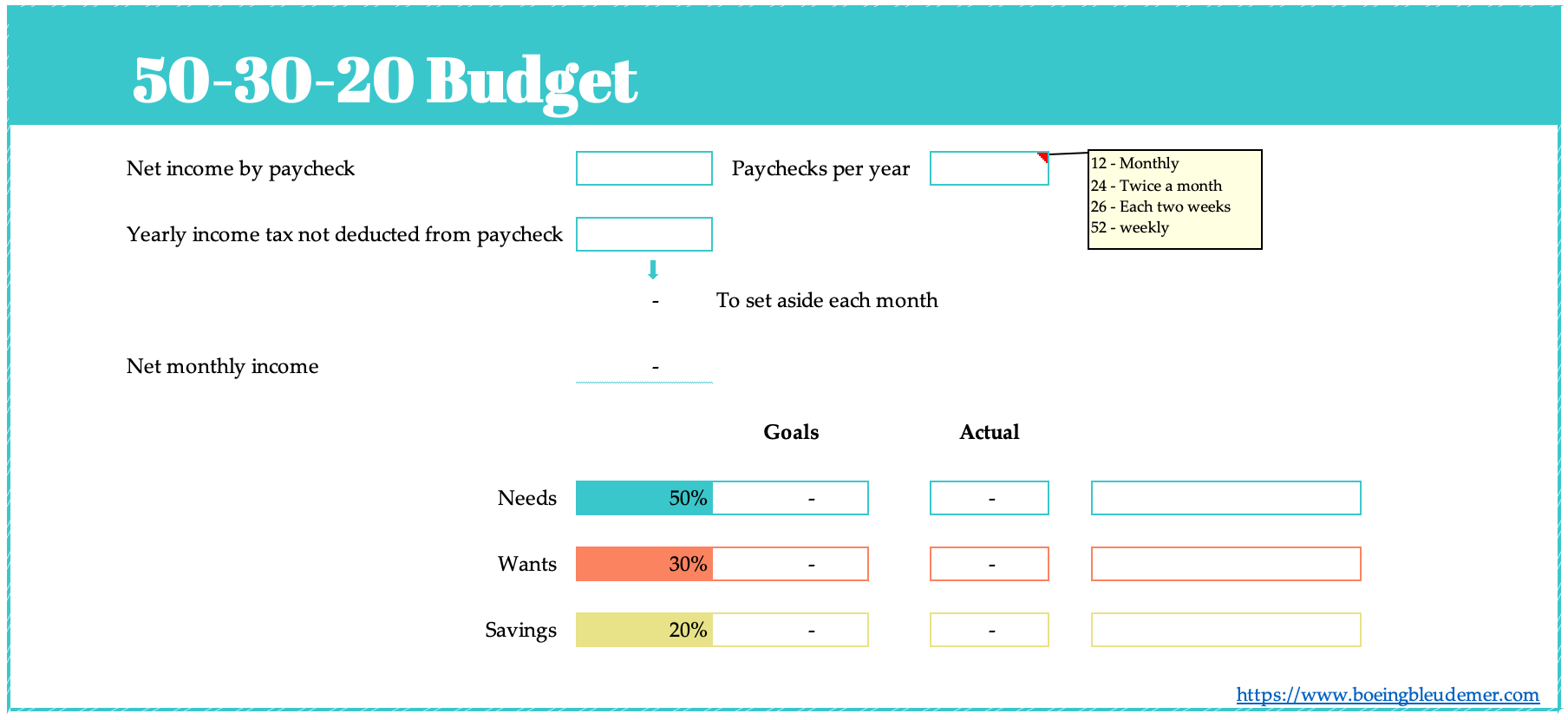

50/30/20 budget calculator

Our 50/30/20 calculator divides your take-home income into suggested spending in three categories: 50% of net pay for needs, 30% for wants and 20% for savings and debt repayment.

What is the 50/30/20 rule?

The 50/30/20 rule is a popular budgeting method that splits your monthly income among three main categories. Here’s how it breaks down:

Monthly after-tax income. This figure is your income after taxes have been deducted. It’s likely you’ll have additional payroll deductions for things like health insurance, 401(k) contributions or other automatic payments taken from your salary. Don’t subtract those from your gross (before tax) income. If you’ve lumped them in with your taxes, you’ll want to separate them out — subtract only taxes from your gross income.

50% of your income: needs. Necessities are the expenses you can’t avoid. This portion of your budget should cover required costs such as:

- Housing.

- Food.

- Transportation.

- Basic utilities.

- Insurance.

- Minimum loan payments. Anything beyond the minimum goes into the savings and debt repayment bucket.

- Child care or other expenses that need to be covered so you can work.

30% of your income: wants. Distinguishing between needs and wants isn’t always easy and can vary from one budget to another. Generally, though, wants are the extras that aren’t essential to living and working. They’re often for fun and may include:

- Monthly subscriptions.

- Travel.

- Entertainment.

- Meals out.

20% of your income: savings and debt. Savings is the amount you sock away to prepare for the future. Devote this chunk of your budget to paying down existing debt and creating a financial cushion.

How, exactly, to use this part of your budget depends on your situation, but it will likely include:

- Starting and growing an emergency fund.

- Saving for retirement through a 401(k) and perhaps an individual retirement account.

- Paying off debt, beginning with high-interest accounts like credit cards.

Get more help with monthly budget planning

For more budgeting advice, including how to prioritize your savings and debt repayment, review our tips for how to build a budget and utilize our financial calculators. Then, consult our personal finance guide.

Not sure how to start budgeting? Downloading a budget app or personal finance software may help, or get informed with a budgeting book.

Or become a NerdWallet member for free. We’ll track your spending in one place and identify areas where you can save.

Read & Write : write for us